Good evening folks!

I was sitting here the other day thinking of my goal to buy me self a home for my family within next summer (2022). There is, however, a challenge here – we really need to move within a year. As of your understanding my fiancé tested positive on her pregnancy test in December. That means that we need to move because we only have two bedrooms in our apartment, and we need three bedrooms since we expect our son number 2 in early august.

Based on the latter our savings rate needs to be high, extremely high. We are talking about a savings rate of 50% of our salary. That means we must live way below our means. Everything we do needs to be carefully considered in terms of buying food, clothes, gifts (to family members) and other consumables (that we really need). We need to review EVERYTHING!

Me and my fiancé sat for hours, even days to figure out how we could minimalize our spending. I can tell you; we finally made a blueprint out of it. A blueprint that will take us from A to B and let us achieve our goal in buying a house for our family. Do you know what was crucial for our plan? That is what you are going to learn in this post.

Here is me and my beautiful fiancé on 17th of may (national day of Norway). We are in this saving plan together! Make sure to have a partner in life!

The good and the bad! More specifically, I am talking about good- and bad dept (not me being good and my fiancé being bad - thats another story 😂). Simply put, good debt makes you rich, and bad debt makes you poor. In other words, good debt makes you money and bad debt takes your money. As I was reviewing my debt, I found that I had a lot more bad debt than I was aware of. So, the first we were set out to do was to get rid of the bad debt, and I am going to show you the best way to do it in this post (in my opinion).

Let me just enlighten what I mean about good and bad debt in more detail. Good debt would be if you where to take up a loan and buy a rental property where your tenants pay rent, and the rent will cover your mortgage and expenses. This puts money in your pocket. Bad debt on the other hand is more like a car loan or a credit loan for when you bought that 60 inches HDR screen. These evil sons of b*****s take money out of your pocket. You should treat bad debt the same way you treat your mother – with a lot of respect. If you do not respect the power from the bad debt, you will make yourself extremely poor.

So what we did was to write down every single bad debt we owe. This included credit cards, school loans, car loans, “family members loans” and my personal residence. Yes, for your information your personal residence is not considered an investment. We are dealing only with bad debt and bad debt is debt that you pay for. Good debt is debt that someone else, such as your tenants, pay for. Hence, me and my family have a lot of bad debt (when considering our own residence as well). Note that the numbers given is just “made up numbers”. Does not matter what the number is, it does not change anything of what I am showing you and what you will learn here. 😁

When you have sorted out your bad debt and wrote down every single post, you are ready to move on to my blueprint for the elimination of bad debt. I have done a lot of calculations to come up with our monthly payments but if you follow my guidelines closely, you will be amazed at how quickly you will eliminate each debt, one by one, from the list you created. Me and my fiancé will be out of bad debt within 8 months (excluded our personal residence in this example – lol).

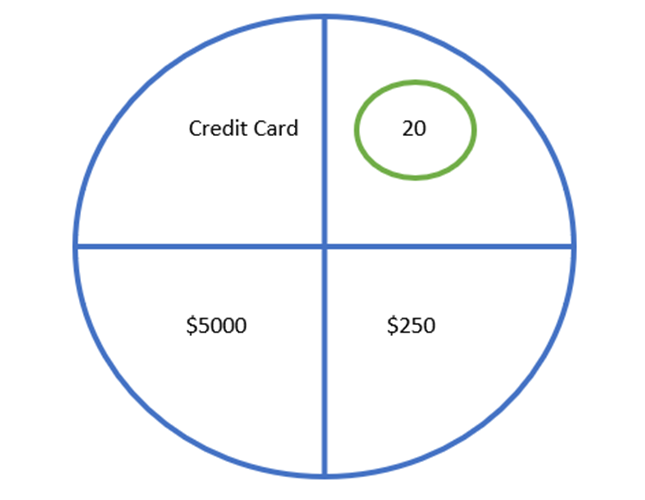

The first step is to draw a visual picture of each bad debt that you have just to contextualize everything and make it easier to get an overview. From there, you can then determine which order each debt will be paid off. The following will show you how you do that.

For each debt you would draw a circle like this:

In the upper left column, you write down your debt post. In the lower left column, you write down the total that you owe. In the lower right you write the minimum monthly payment. Divide the total number you owe by the minimum monthly payment. Write this number in the upper right column and circle it with green. The circled number are the number of months it will take to pay of that specific debt. Do the same thing for every bad debt in your list, e.g., car loans, school loans etc.

The next you want to do is to determine the order you want to pay off each debt. When you have listed all your debts find the lowest number and write “number 1” next to that debt. Find the next lowest number and write “Number 2” next to the debt etc. For example, if the smallest circled number you find is $20 (like in the picture above), then you would write “Number 1”. This is the first bad debt that you will eliminate.

Why should we not pay off the debt with the highest interest first? The most important thing here is that you see som fast results, and that is my case here. It is also easy to get discouraged here and quit before even paying of one of your debt, so it is also more of a motivational thing. By paying of the lowest debt first you are also paying off the debt that will be the quickest to pay off – hence results show up faster. This visibility keeps your head in the game, and you manage to focus on your job further on. You also have a clear outline of every debt you owe and the order in which you will pay off your debts (The plan).

My favorite and what really makes the differences; find an extra $100 each month besides work. If I cannot come up with an additional $100 each month, what do you think will happen with our house? The goal will not be reached, that's for sure! So buckle up and join me in this goal to get an extra $100 a month or more just to be on the safe side! It’s a great and meaningful challenge for yourself! Mark my words.

Then, except for your “Number 1” debt, pay only the minimum monthly payment for the other debts you might have. For this blueprint to work properly pay only the minimum monthly payment due on each debt and put that extra $100 towards debt “Number 1”. Therefor, for debt “Number 1”, you are paying the minimum monthly payment + $100 shiny USD! Continue to do this until “Number 1” is eliminated – then throw a party at your friend’s house!

Not as a surprise but now we move on to debt “Number 2”. Except for debt “Number 2” you only pay the minimum monthly payment on the other debts. Now here is the big difference, for debt “Number 2”, pay the minimum monthly payment required + the full amount you were paying on debt “Number 1”. For example, on debt “Number 2” you pay the minimum monthly payment required, the minimum monthly payment you were previously paying on debt “Number 1” and the additional $100. By doing so with each debt you pay off, you will be accelerating your payments on the next debt. Continue each month until debt “Number 2” is paid off. Continue this process for each debt and boom your “bad debt free”.

As I wrote earlier if me and my fiancé follow this blueprint, we will finish off in just around 8 months. This, I can tell, is over $20 000 of bad debt. I will also tell you guys that the magic behind this blueprint is really an extra $100 per month. If you stick with this, you will be amazed at how quickly you can get out of bad debt. When you are free of bad debt, invest everything you paid on your bad debt into HIVE (joke, you do whatever suits you).Of course, this is also a bit stressful because for this to work and for us to reach our goal we got to stick to it every month. If we skip only one month, then the chances are, we will begin a habit of not following the process and our goal will be lost. Full focus and the goal will be achieved. I hope I can give you all a positive post next summer showing you that we reached our goal as a family!

This is it, our blueprint! I hope you enjoyed it and can get use of it somehow, we will definitely! For my last words always ask yourself this question when taking up debt: Will this debt pay me back more than what I put in? It will change your world, it changed mine.

Have a happy HIVE day!

Cheers

-Olebulls

Love the simplicity and the visualization. Banks, brokers & Co. make it sound sophisticated and complex to confuse people on purpose. Looking forward to your post celebrating the achievement of your goals as a family.

Ye you are totally right, they do... I am here to make it simple :)

Great I hope I see you here next year @kriszrokk!

Posted Using LeoFinance Beta

That's the most Norwegian-looking couple ever shared on Hive, that's for sure! 😎😆

Like the simple idea behind this approach. Simple rules usually beats complex analysis and attempts to tryhard in the long run. I've never had any form of debt whatsoever, so can't really relate though :p

Hahah fo sho Freddy!

yup, I like it simple! and keep that up my friend, stay out of bad debt!

Posted Using LeoFinance Beta

Good luck with you on accomplishing your goal! I know for us when my wife and I first got married one of the best things we did was to get a balance transfer loan. We were able to get a loan with a 4% interest rate. That loan was big enough to cover all of our other bad debt. That way instead of multiple payments to places with over 20% interest, we were able to pay much less to only one place. In fact, the rate on the loan was so low that we were able to pay more than the minimum payment and it was still less than our previous payments. It was five year loan and we had it paid off in 3. It was a great feeling.

Posted Using LeoFinance Beta

Wow that's nice @bozz! That is actually a pretty good idea - thanks! So if I get of my track and miss out on some payments I can hopefully get a loan big enough to cover the rest of the bad dept! Nice man, think I will sleep better now hehe

Posted Using LeoFinance Beta

Yeah, when we got married we had some combined credit card debt from about three or four cards that had interest rates over 20 percent. We paid off all of those with the balance transfer loan and then destroyed the cards. We left the accounts open so it wouldn't impact our credit, but with the cards gone we could no longer use them. Then the focus was solely on the Balance Transfer Loan. We got it through our credit union. Took care of $20k in combined debt like magic!

Posted Using LeoFinance Beta

Wuhu, that is some real magic man! Thanks for sharing this - information weighted in gold!😃

Congratulations @olebulls! You have completed the following achievement on the Hive blockchain and have been rewarded with new badge(s) :

Your next target is to reach 300 upvotes.

Your next payout target is 500 HP.

The unit is Hive Power equivalent because your rewards can be split into HP and HBD

You can view your badges on your board and compare yourself to others in the Ranking

If you no longer want to receive notifications, reply to this comment with the word

STOPCheck out the last post from @hivebuzz:

Support the HiveBuzz project. Vote for our proposal!