Merry Chrismas, degenerettes and degens!

When I first started my crypto journey I often found myself saying, "I would have bought that if I've had more fiat". During an uptrend or a full-blown bull ride, good opportunities slip through our hands and that's quite normal, can't have them all, right?

Lending and borrowing can be a solid choice if you are certain that the uptrend will continue and don't want to miss a chance but instead maximize your profits. Also, if you've already invested in an asset you don't want to split up, you can use it as collateral to get liquid and earn some interest on it as well.

In last week's issue of DeFi Dives I was writing about Marinade, a staking platform on Solana and also briefly mentioned the lending and borrowing platform MarginFi. Today I'm going to share my lending & borrowing strategy using both platforms to maximize my gains.

Let's start with Marinade where I staked some $SOL using the liquid staking option.

I staked SOL to earn an annual percentage yield (APY) of 7.88% which isn't that much but the best part is I received a mSOL receipt that represents my stake and which I can use for whatever purpose I want while it's still earning APY.

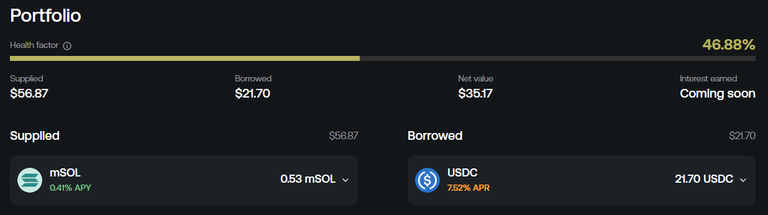

I then headed to MarginFi where I supplied(lent) mSOL and received an additional APY of 0.41% on top of the 7.88%.

Now that I have supplied mSOL I can use that as a collateral and borrow other assets against it. For example, I borrowed USDC which has an APR of 7.52% which isn't so high in my opinion, a good thing since obviously the interest is growing on the borrowed amount, meaning I will have to pay back a bit more in the future.

Here in the picture above is also shown my Health factor. This is the relation between the amount of the asset I've supplied and the amount of borrowed asset. It's important to not let it go to zero or below because then you are exposed to liquidity risk.

I'm actually on the safer side now as my health factor has grown quite a bit because the price of SOL has increased.

It also determines how much more you can borrow using your collateral. For example, about a week ago I could've borrowed an additional $3(already borrowed $21) but since the SOL price has gone up, so has the amount I can now borrow which is currently at $9.

Some Notes

All assets have their own weight percentage, so you might not be able to borrow 100% USDC against the crypto you have lent.

Even though Solana has very low fees, the signing of the supply contract fee was a bit higher, less than 1$ still.

Besides the health factor, it's a good idea to check the liquidation price of an asset you are lending. For mSOL it is $56.60 while its current value is $110.26.

Plans

So what to do with the borrowed USDC?

One way could be to repeat the process, swap USDC to SOL, go to Marinade & stake, and supply more mSOL to increase APR and the amount to borrow.

I haven't abandoned this idea but what I did was I bought some other tokens on Solana and traded them back and forth to increase my USDC stack.

At the moment I have almost doubled my loan but I'm not planning on paying it back any time soon. Here's why.

MarginFi has a points system that counts toward an airdrop while both activities, lending and borrowing, add to the total points.

- Lending earns 1 point per dollar lent per day.

- Borrowing earns 4 points per dollar borrowed per day.

Points are refreshed once in 24 hours and if I should repay the loan, I wouldn't be earning the borrowing points any more. Since the USDC APR is low and therefore growing the borrowed amount slowly enough, I've decided to keep it open and watch the airdrop through.

There are no guarantees that my points will be enough to count for the airdrop or should the drop be just crumbs for small timers like me. In any case, I now have more chips to play with.

Some Notes

At the moment, the Solana ecosystem has some kind of airdrop craziness going on. Some are finished, some are ongoing and some are just rumours. So if you decide to loop your assets, it might be a good idea to check other platforms as well. Kamino Finance, for example, is another Lend/borrow one.

Here's a Solana airdrop checklist. Remember to do your own research. At least Jupiter and MarginFi are ongoing.

Conclusion

Lending crypto and borrowing stablecoins is a pretty good strategy when the trends are pointing upward. As the crypto assets increase in value, the risk of getting liquidated gets lower and it also gets much easier to repay the loan.

In addition to this, you will have stables that you can use to create loops to maximize your earnings if you believe the uptrend will continue and hunt those airdrops while doing so.

Of course, none of this is new and there are many other lending/borrowing platforms such as Compound, Aave, etc, and you can obviously apply the same strategies to those.

As for me, the hype on Solana and especially the airdrops that incentivize the activity even more make it a chance I'm willing to take. Also, the low fees on Solana allow to play this with smaller amounts and for a shorter time.

Thank you for reading!

DISCLAIMER: There is a risk of getting liquidated. Remember to DYOR.

Thumbnail background image made with Canva

Posted Using InLeo Alpha

Yay! 🤗

Your content has been boosted with Ecency Points, by @brando28.

Use Ecency daily to boost your growth on platform!

Support Ecency

Vote for new Proposal

Delegate HP and earn more

Congratulations @brando28! You have completed the following achievement on the Hive blockchain And have been rewarded with New badge(s)

Your next target is to reach 11000 replies.

You can view your badges on your board and compare yourself to others in the Ranking

If you no longer want to receive notifications, reply to this comment with the word

STOPCheck out our last posts: