Blockchain is a word that can mean many different things.

Blockchain is a word that can mean many different things.

For developers, it is a set of protocols for storing data on a distributed network. For crypto enthusiasts, it is the technical backbone of the new wave of digital currencies. And for revolutionaries, it is a tool for creating a radical new decentralized society.

However you see it, the basic idea is simple enough — a distributed ledger.

This can be explained using the friendly metaphor of a classroom.

Imagine that you have a classroom full of people, and every single person in that classroom has a copy of the same notepaper.

Every time an event happens, or a transaction is made between any of the people in the room, it is simultaneously noted down on everyone’s notepaper, which is referred to as the ledger.

This is the essence of blockchain — an immutable shared record of transactions.

Just like that, but digital, and distributed.

It is this simple idea that has captured the imagination of the world and has potentially profound implications.

The essence is trustlessness. For for the first time in human history, people can place trust not in god, not in each other, not in institutions, but in data.

This allows the formation of a global collaborative network without centralized formal institutions,

that uses cryptography and computer code in the place of centralised management — preventing the possibility of theft and fraud.

Origins

Satoshi Nakamoto, the world’s most enigmatic billionaire

The first blockchain was designed in 2008 by an anonymous person or group known as Satoshi Nakamoto, who put forth the idea in a white paper that called it ‘bitcoin’.

The idea is thought to have arisen in response to the bad behaviour of the banks that precipitated the financial crisis, and the desire to have a sovereign currency which could not be so easily manipulated.

Thus, a peer-to-peer electronic cash system was born. The first digital currency which through the blockchain was able to solve the ‘double spending problem’ without the need for a trusted authority.

Although bitcoin was the first implementation of the technology, the idea of blockchain took on more significance later when the same technology was used in other applications.

Technicals

A chain of blocks

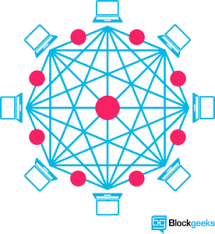

It was the genius of Satoshi Nakamoto to combine cryptography with distributed computing — both technologies that have existed for decades, into a new model where a secure database is shared between a network of computers.

The shared database is a string of blocks, each block being a record of data — a ledger that is encrypted and given a unique identifier called the hash miner.

Computers on the network, known as nodes, validate transactions as they occur and add them to the block that they are building, before broadcasting it to other nodes so that each node has a copy of the exact same database.

Because there is no centralized component to verify the changes to each database, and make sure that they all remain the same, the blockchain uses a distributed consensus algorithm in order to create agreement between each node that the same entry is being made to each ledger, meaning that no node can create an entry on the ledger without the agreement of others.

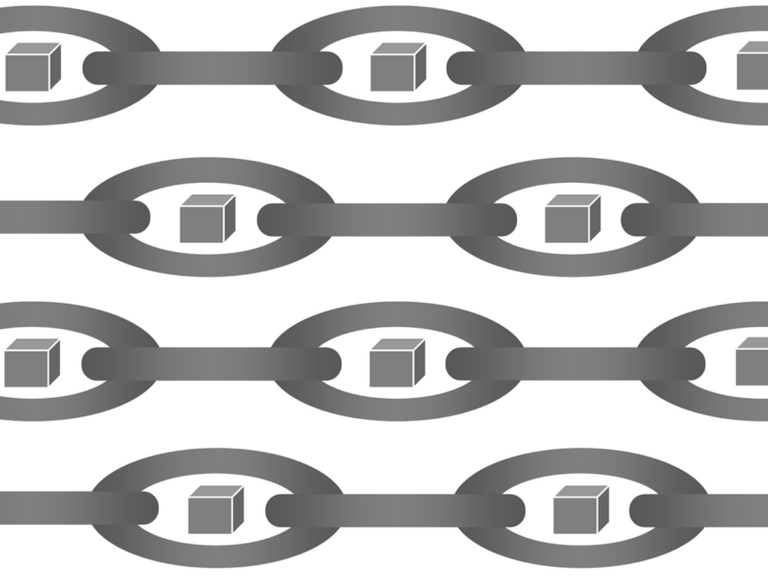

Each time a block gets completed a new one is generated, until there are a countless number of blocks in the blockchain all connected to each other by links.

The blockchain was designed so that transactions are immutable — they cannot be deleted.

each block contains a hash value that is dependent upon the hash of the previous block, meaning that if one is changed, then all the other blocks linked to it will be altered.

So there we have it, the blockchain on its most basic level can be understood as a new kind of database made up of distributed ledgers that form a consensus of synchronized digital data, without centralized administration!

Smart Contracts

Smart contract: A digitally enforceable contract

The second generation of blockchains are what have really created revolutionary fervor.

The basic blockchain evolved from a system of distributed ledgers, to become a fully fledged globally distributed cloud computer. That is, the ethereum virtual machine.

This is achieved by adding a second layer of functionality to the blockchain, that offers the possibility to automate the working of the networks.

This functionality is called smart contracts, digitally enforced self-executing contracts, with the terms of the agreement or operation directly written into lines of code which are stored and executed on the blockchain to be triggered by certain events.

These contracts can be used for automating basic operations on the network, removing the need for a trusted third party.

An example smart contract might be a contract that allows you to send ethereum automatically on a certain date, sort of like a direct debit, except automated, open and transparent. The user would simply create a contract, and push enough ethereum to the contract so that it can execute the command.

Every transaction that is made through the smart contracts is recorded and updated on the blockchain, which keeps everyone involved with the contract accountable for their actions.

This transforms the blockchain from more than just a database into a whole new way of storing, organising, transferring, and communicating between the parts of a distributed organisation.

Ethereum has been very successful attracting a large and dedicated community of developers and enterprises that have developed the capacity of the network by building decentralized applications, and turning a simple blockchain into a distributed virtual computer.

Tokens

Ethereum tokens are another application of the smart contract — quantified units of value that can be passed between ledgers, and which can fulfil all kinds of different functions.

These tokens can represent anything from real commodities like gold (Digix) to currencies used in future blockchain ecosystems, like Status (SNT).

Tokens can have an endless number of use cases, as demonstrated by the 80,000+ tokens on the Ethereum network, and are commonly used for crowdfunding in ICOs.