The concept of Impermanent Loss is comically misunderstood

Back in summer 2021 I did a deep-dive on this idea of "losses" in relation to being an AMM liquidity provider and it took me many hours of research to figure it all out. The reason why it took so long had nothing to do with impermanent losses being a complicated idea, but rather the fact that every single source that attempted to explain it was doing it incorrectly.

I proved this beyond any doubt in the original post by searching for the keyword "arbitrage" within the given "official" explanations. This keyword appeared within every single article, which heavily implies that these people have no idea what they are talking about. Why? Because this type of slippage occurs exactly the same no matter how many markets or liquidity pools there are. How can arbitrage be a factor if there is only one liquidity pool and thus zero opportunities to arbitrage another market? Make it make sense.

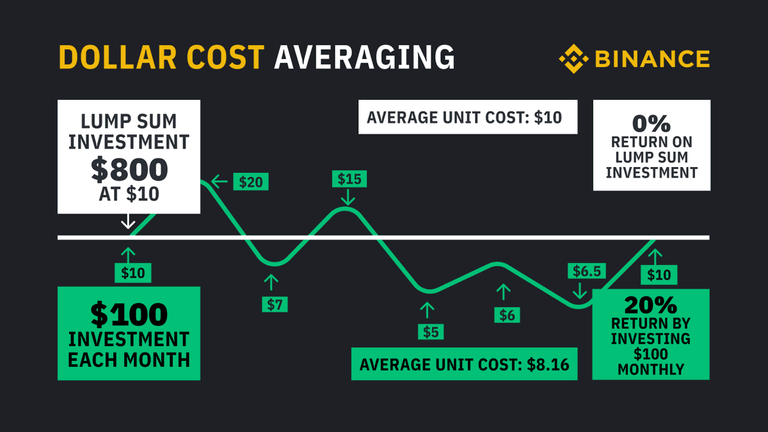

The very naming convention and usage of the word "losses" is born of degeneracy. No one would ever claim that dollar cost averaging is an "impermanent loss". I will prove in this post that impermanent losses are actually a subset of dollar cost averaging. Anyone who dollar costs averages in this extremely specific way (constant rebalancing) will get the exact same result as impermanent loss within a liquidity pool.

(IL == DCA)

The idea behind DCA is that it lowers volatility so that the investor won't go on tilt by lump-sum shoving their entire stack into a market only for it to immediately dump on them. It's a basic form of calculus in which we hope that there's more area below the buying curve than above it. IL is the exact same thing, except it's superior in a lot of ways because the DCA is algorithmic and happens on every single swap within the pool. It's completely automated, and it's the traders (swaps) who pay all the fees; fees that in turn are paid to the DCAer (LP).

Giving a nice clean example.

The example I'm going to give is a person holding 1 BTC paired to 100k USDT inside a liquidity pool. During this time, BTC will increase from a price of $100k per coin to $400k per coin. The numbers on this example work out quite cleanly, after everything is said and done the user has been DCA selling their Bitcoin into USDT because the value of Bitcoin is going up. They start with 1 BTC and 100k USDT and end with 0.5 BTC and $200k USDT.

But OMG such losses bruv!

Of course when degenerates look at this they are going to ask stupid questions like, "Well what would have happened if he had just held the 1 BTC and 100k USDT outside the pool?!?" The user would still have 1 BTC and 100k USDT for a total value of $500k. The user has "lost" $100k due to these mythical "impermanent losses". Sure bud, sure.

Now let's compare to DCA.

Again the user is going to start with 1 BTC and 100k USDT... and every time BTC spikes up more they are going to rebalance their position to even it out.

- Starts with 1 BTC and 100k USDT

- At $175k the user sells 0.21428571 BTC ($37500)

- 0.78571429 BTC / $137500

- At $250k the user sells 0.11785714 BTC ($29,464.28)

- 0.66785715 BTC / $166,964.28

- At $325k the user sells 0.07706045 BTC ($25044.65)

- 0.59079670 BTC / $192,008.93

- At $400k the user sells 0.05538718 BTC($22,154.88)

- 0.53540951 BTC / $214163.81

HM! PRETTY DAMN CLOSE!

In the case of manual DCA the user "lost" $71,672. If they had just held the 1 BTC the entire time they'd have that extra $72k. Meanwhile, the AMM algorithmic DCA was down $100k vs hodling. Chalk up this difference to the fact that the AMM position was selling constantly while the manual DCAer only sold 4 times (and one of those times was at the tippy top). The AMM position has 0.5 BTC left while the manual position has 0.535 BTC left out of 1 BTC total. Again, pretty close.

What we didn't factor in is how much yield the automated market making liquidity pool provider made. This massive move from $100k BTC to $400k BTC would have probably had a lot of ups and downs and a lot of income generated for the LP. It would not be that hard for the LP position to outperform the manual DCA seller, especially once we factor in trading fees. Assuming this trading session lasted a year and the LP position earned 14% APR: both strategies would be perfectly even.

The main point that needs to be made here is that the manual DCA trader is considered to be "taking gains" and "creating hedged and responsible positions" while the AMA LP investor is "taking losses". I feel like I shouldn't have to explain further how stupid that is. They are the EXACT SAME STRATEGY. If the DCA trader rebalanced their position every day (or even every week/month) they'd end up with significantly less than the LP investoooor due to the difference in yield/fees. It's also just a great way to lower the risk of a volatile alt by pairing it to BTC. USD doesn't even need to be in the equation.

Conclusion

The only difference between rebalancing a portfolio with dollar cost averaging and impermanent losses in a liquidity pool is how many times the mathematical operation occurs. With manual trading this is done as many times as the user makes a trade. With AMM it's done automatically via algorithm on a perfectly smooth [k = x * y] curve.

The decentralized nature of an automated market maker flexes superiority over the centralized version. At some point the chance that a centralized exchange collapses will be much greater than an attack on decentralized liquidity. Once that happens DEFI will be superior to alternatives in almost every way.

If you, as an investor, believe that DCA strategy is a valid for reducing volatility and playing it safe (as is the standard investment advice) then you cannot allow anyone to try and trick you into believing that impermanent losses are in some way different than this tried and true financial strategy.

Impermanent losses have absolutely nothing to do with arbitrage, and anyone who believes it does is misinformed. A liquidity provider unsurprisingly: provides liquidity. That means they are selling when the market is buying and they are buying when the market is selling. Take the other side of the trade.

I'm often scared of IL and just recently started knowing about it with the Leo pool but it's mainly because I'm not well informed, so what really matters is how many transactions happen at the pool and you as a liquidity provider can still be ahead of the game since it's all done by the algo? 🤔

The question you have to ask yourself is pretty simple:

or

If you want the moonbag then an LP is a bad idea unless you believe that both assets are going to moon. In the case of LEO/HIVE or LEO/CACAO both could indeed easily moon together. Anything paired to USD is a much safer bet, with volatility being reduced by a square-root.

In the example I gave in the OP BTC went x4 but their LP position only went x2.

The same would also be true of Bitcoin collapsed 75%.

The LP would only be down 50%.

Not only that but the LP is still 50% USD so you can liquidate the position after a crash like that and just ape all the USD into BTC and buy the bottom to turn it into a moonbag.

And none of this factors in the yield that the LP is generating.

Well explained. I'm impressed.

Yeah, I think I know what you mean. That's interesting, I wasn't really aware of that. I keep your article because I think that as long as I'm not able to explain it, I don't really understand.

Thanks again for this valuable article!

Thank you for this explanation.

!BBH

@edicted! Your Content Is Awesome so I just sent 1 $BBH (Bitcoin Backed Hive) to your account on behalf of @logen9f. (12/20)

One of the best IL explanations I've read so far! 🙂 !BEER

This is a brilliant perspective, and helped me a lot.

Glad to hear it...

I was thinking it might be redundant because I've already blogged about this topic a couple of times.

But that was a long time ago and this is a different angle with a real example.

View or trade

BEER.Hey @edicted, here is a little bit of

BEERfrom @pardinus for you. Enjoy it!Do you want to win SOME BEER together with your friends and draw the

BEERKING.