CBDCs, IMF's New Bretton Woods, WEF's Great Reset - Where is it all headed? (Part 1)

Image source

Governments will destroy markets long before they figure out how they work. - Ludwig Von Mises

Introduction

I chose the (mostly paraphrased) quote above to place the reader's mindset in this specific context. Governments and Central Banks are indeed slow and ineffecient, no doubt about it. And in this current financial and monetary paradigm shift that is evolving at warp speed, their ability to lead innovate, or even keep up for that matter, will put them at a disadvantage and give humanity a window of opportunity to take the power back away from them; the power they have held for centuries.

Sadly though, we know that those who are currently behind the design of CBDCs (Central Bank Digital Currencies) and who will implement them will undoubtedly use them for continued crafty mass looting and for other nefarious purposes - mostly in terms of additional power grabs.

This post will be structured as follows:

PART 1:

- CBDCs (Central Bank Digital Currencies)

- IMF (International Monetary Fund) & IMF's New Bretton Woods

- BIS (Bank for International Settlements)

- Regional & Country-specific Notes of Interest

PART 2:

- Thoughts and Predictions on this Global Monetary Reset

- Final Thoughts

CBDCs (Central Bank Digital Currencies)

What are CBDCs?

Central Bank Digital Currencies, or CBDCs as they are now more commonly referred to, sometimes get misunderstood as countries' respective digital fiat currencies (i.e., the digital deposits of dollars, euros, yen, etc. in depositors' bank accounts). CBDCs are not this.

Rather, CBDCs are digital currencies that countries propose to replace their current cash, coin, and digital entry systems which would thenceforth entirely reside on a centralized or decentralized blockchain; moreover, people and companies would hold the digital currency in their digital wallets, make digital payments for the purchase of goods & services, transfers, etc.

Cash may be still be used during the transition period when countries migrate toward 100% CBDC-only usage. Of course, this will still take a few to several years to fully implement. But, like it or not, it is inevitably coming our way.

What exactly is coming our way?

Governments and their Central Banks have no choice. They probably would have preferred to avoid or delay this turn, but as financial technology (FinTech) and cryptocurrency & blockchain technologies have been advancing at a very rapid stage since the advent of Bitcoin in 2008, they have to keep up with the times, lest they embrace their own demise.

There's a fantastic article entitled Central Bank Digital Currency, A Growth Or Financial Repression Tool? (alternate link via ZeroHdege) written by Daniel Lacalle that nicely describes the current state of affairs of this conundrum. At the begining of the article, the author demonstrates how the arguments for CBDCs actually don't make too much sense, as they are actually not in line with their stated mandates and objectives. The author is right. Here are a few excerpts which nicely encapsulates the redundancy of it all:

Central banks will not make their digital currencies a success if citizens fear -as they do- that the policymakers will constantly strive to dilute the purchasing power of the currency, which means less purchasing power of economic agents’ salaries and savings.

The process of any asset becoming a widely used currency is the most democratic there is. It cannot be decided by governments and cannot be imposed. If governments and central banks push financial repression and devaluation of their currency, citizens will move to other means of payment that become real money. Cryptocurrencies have not developed because of people´s idiocy or ill-means, but because of the lack of trust in fiat currencies and the constant desire of central banks and governments of destroying the currency to disguise structural problems.

When he says: "If governments and central banks push financial repression and devaluation of their currency, citizens will move to other means of payment that become real money." he is right.

That is exactly what I think Central Banks will end up doing and it will push the masses to use sound and honest alternatives instead, namely decentralized cryptocurrencies like Bitcoin and others that are not in the control of governments or central banks and cannot be debased (i.e., their supply cannot be increased on a whim as central banks have continuoulsy done throughout their existence).

The author continues:

That is why a central bank digital currency is an oxymoron, a contradiction in terms. The reason why citizens demanded cryptocurrencies is precisely because they were not controlled by central banks that constantly aim to increase the money supply and generate depreciation of money, inflation.

The article is worth reading in its entirety.

What are some characteristics currently under consideration by Central Banks for their CBDCs?

Without getting into very long and arduous central bank white papers and briefings, here are some initial characteristics CBDCs would seem to have:

They would most likely reside on a centralized blockchain ledger

Their supply though initially fixed at a certain quantity would have the possibility of being increased (unlike say Bitcoin that has fixed supply of 21 million coins)

Every single transaction can be checked, monitored (traced & tracked) and taxed directly. No anonymity or privacy!

Each wallet to hold the digital currency would have to be identifiable (personal digital IDs for citizens and some other digital ID for companiess, organizations, and other entities).

Digital IDs of wallet holders will most likely be tied to centralized national databases (health & tax authorities, among others).

They could easily usurp Fiscal-policy making from governments. (i.e., the CBs can deposit digital currency directly into citizens' wallets.)

They could be considered as assets rather than liabilities (debt).

??? (other characteristics to come, as they are all currently in the design stage)

There are still many uncertainties left for CBDCs.

Could there be any benefits to CBDCs?

These considered, I would, nevertheless, like to note that there can be real advantages and benefits for common citizens with the issuance of CBDCs. In other words, CBDCs may not be all threat depending of course on how CBs choose to deploy them.

Will ordinary folk have a say?

And a lot of this will depend on the extent to which citizens make themselves integral to the process; there has to be some pushback, otherwise CBs will do as they usually do and set themselves up to loot at will, as they always do.

Yeah sure they always have these "public consultations" but we know that these are ignored 99.99% of the time. Maybe this time will be different (cough cough).

Additional Analysis

Here is a good video that provides a good introductory summary to what CBDCs might entail for which I have also added some user comments for additional insight:

- Video: Coinbureau - Coinbureau - CBDCs: Good or Bad for Crypto?? (Oct 18, 2020)

At around the 20:22 mark of this video, Coinbureau's Guy makes some sobering predictions:

"What I fear is that CBDCs will be used as a tool by governments around the world to track every single thing that you do. And, if they don't like it, they will simply connect it to your digital passport, switch off your money, and your right to leave the country. This sort of system could also be used to force people to prove that they don't have the [corona, or other given] virus, if you want to participate in the non-lockdown economy...The powers that be could implement a policy whereby your passport doesn't work until you have had the vaccine."

All this is indeed sobering to even contemplate. But I've extensively documented (see CovidPass - The Technocrats Wet Dream for mass enslavement and submission and International Air Travel to require COVID-19 Test or Vaccine | Immunity Passports) this nefarious shit beforehand on how they do indeed plan to implement this beast system. And this is already being trial-runned in the UK and elsewhere.

Also, travel restrictions are like a form of capital control, but ones of human capital control, i.e., preventing citizens from leaving their own countries - something which I have predicted would eventually happen nearly a decade ago.

Here are some noteworthy user comments from the viewers of this video:

CBDC take the most efficient scam in history and supercharge it to the nth power. -Reuben Germain

Agreed. The additional power Central Banks (note I don't say Governments) can acquire with CBDCs will be unprecedented and exponentially more over-arching.

All Beast system has to do is cut off any port that allows transfer back to fiat (banks) and Crypto exchanges die. - Gary George

This is true in theory, but unlikely in practice. Think Game Theory...

They will need to tie a lot of social benifits to the CBDCs in order to make them more attractive. If they turn out to be all big brother, watchdog restriction coins then people will just hold most of their wealth in other crypto currencies that are none CBDC and just swap what they need to. - Juan Luis Almonte

This is an excellent point. I couldn't agree more. They will have to offer some tangible benefits and incentives for on-boarding the masses, lest they simply force them into the digital enclosure.

They will lure people in by giving out free money (UBI). replied Najeeb Siddiqui in this thread.

Bingo! That will be one way. They other is probably when the national fiat implodes and the digital fiat held in bank accounts will be devalued at 50% or so, it will be then traded-in for X amount of CBDC, take it or leave it!

Another user confirms the former's point:

There won't be any choice! Most people's livelihoods will be wrecked, and the digital UBI will be a lifeline. Principles go out the window when you have a mortgage to pay or kids to feed. - Steed

Indeed. People won't give a fuck when they need to buy food to feed their kids! I need it now! This will be as easy to accomplish by Central Banks as slicing a dull knife through half-melted butter.

With that grim thought out of the way, I'd like to leave the last comment on a more hopeful note:

It's all about power and control from the fed's and the CB's. They want to own you, the world. People's last chance is to unit, rise and fight back the corrupted govt's around the world. We all can do this but the mass need to be educated. If CBDC do roll out, certain cryptocurrencies with useful utilities that provide the foundation for the blockchain revolution will rise unlike BTC and a bunch of others claiming to be a monetary system fighting against the fiat and the alike will be controlled by the fed's and the CB's around the world. This is a new world order, the people don't have a say anymore unless the mass is educated and we rise and reclaim back the financial freedom. Freedom means war and we go to war and that is the only way out. - GlobalEliteXRP XRP

Education is indeed key!

There are still so many unknowns and so much to come regarding CBDCs and how CBs and supranational organizations such as the IMF are going to design and deploy them.

Nevertheless, we can gain a good understanding of where they are headed by examining what they have been spewing as of late.

So, shall we?

Let's begin with the IMF.

IMF (International Monetary Fund) & IMF's New Bretton Woods

In my The International Banking Cabal Exposed (4 Part Series) from three years ago, I outlined how the IMF, World Bank, and BIS - Bank for International Settlements were part of a highly integrated international banking cabal that have financially enslaved the masses for the better part of the last century.

Image source

The IMF (like the BIS) is a supranational criminal organization that has total immunity from prosecution. They have practically zero oversight peering over their shoulders and have implemented extremely harmful policies which they have imposed on governments worldwide with, sadly, very little backlash. I have documented these extensively in my series should the reader wish to venture down those rabbit holes.

Now, they are at it again!

Before we look at the IMF's proposed New Bretton Woods style reset, we must have a quick look at the effects the previous Bretton Woods has had on countries currencies and their purchasing powers.

A recent article from Bitcoin News entitled The Great Financial Reset: IMF Managing Director Calls for a 'New Bretton Woods Moment'

really brings the effects of the original Bretton Woods system in context:

As soon as the Bretton Woods system was up and running, a number of people criticized the plan and said the Bretton Woods meeting and subsequent creations bolstered world inflation. When the IMF and World Bank Group started, a leading editorialist for the New York Times abruptly had to leave his position for writing about the Bretton Woods system’s horrible and negative effects on the global economy.

The editorialist was Henry Hazlitt and his articles like “End the IMF” were extremely controversial to the status quo. In the editorial, Hazlitt said that he wrote extensively about how the introduction of the IMF had caused massive national currency devaluations.

Hazlitt explained the British pound lost a third of its value overnight in 1949.

“In the decade from the end of 1952 to the end of 1962, 43 leading currencies depreciated,” the economist detailed back in 1963.

“The U.S. dollar showed a loss in internal purchasing power of 12 percent,

the British pound of 25 percent,

the French franc of 30 percent.

The currencies of Argentina, Brazil, Chile, and Bolivia lost, respectively, 89, 91, 94, and 99 percent of their purchasing power.”

Are you starting to get a little taste and forewarning about what another Bretton Woods style reset might entail for your pocket book and financial well being in the years to come?

If so, it would be best to keep reading.

Last week the IMF announced that (on the back of the Covid-19 crisis - never let a good crisis go to waste, they say) it was an opportune time to introduce a "New" Bretton Woods style reset/monetary system.

Sure the gig of the old system is on its last legs (particularly since 2008) and though it can chug along for perhaps a few more years, the IMF along with their co-conspirators at the BIS, WEF, and the UN are taking advantage of this crisis to spearhead their new beast financial system of enslavement so that they can continue to loot the masses to further enrich themselves in addition to gaining an increasingly exponential amount of power over our lives for the next several decades to come.

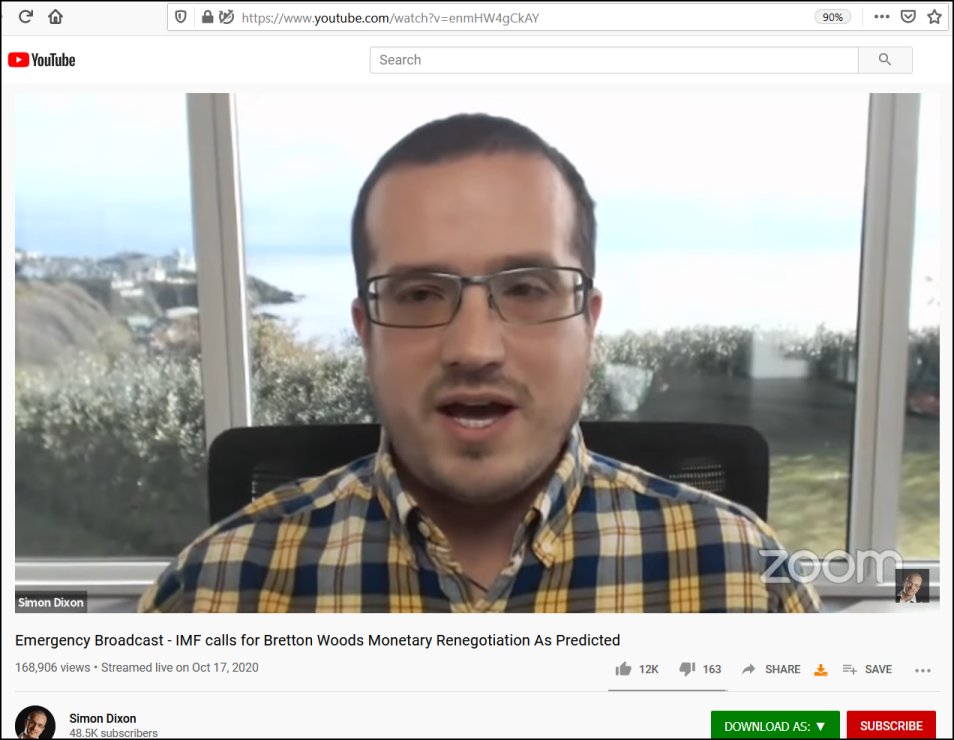

I can think of no better resource to offer you to get the broader picture of this plan (along with a nice summary of the previous Bretton Woods system) than that of a video by Simon Dixon. So, here is the must watch video (in its entirety) to get all the relevant facts and takes on this plan. I strongly suggest you watch the entire video from October 17 entitled Emergency Broadcast - IMF calls for Bretton Woods Monetary Renegotiation As Predicted:

Screenshot & URL of the video https://www.youtube.com/watch?v=enmHW4gCkAY

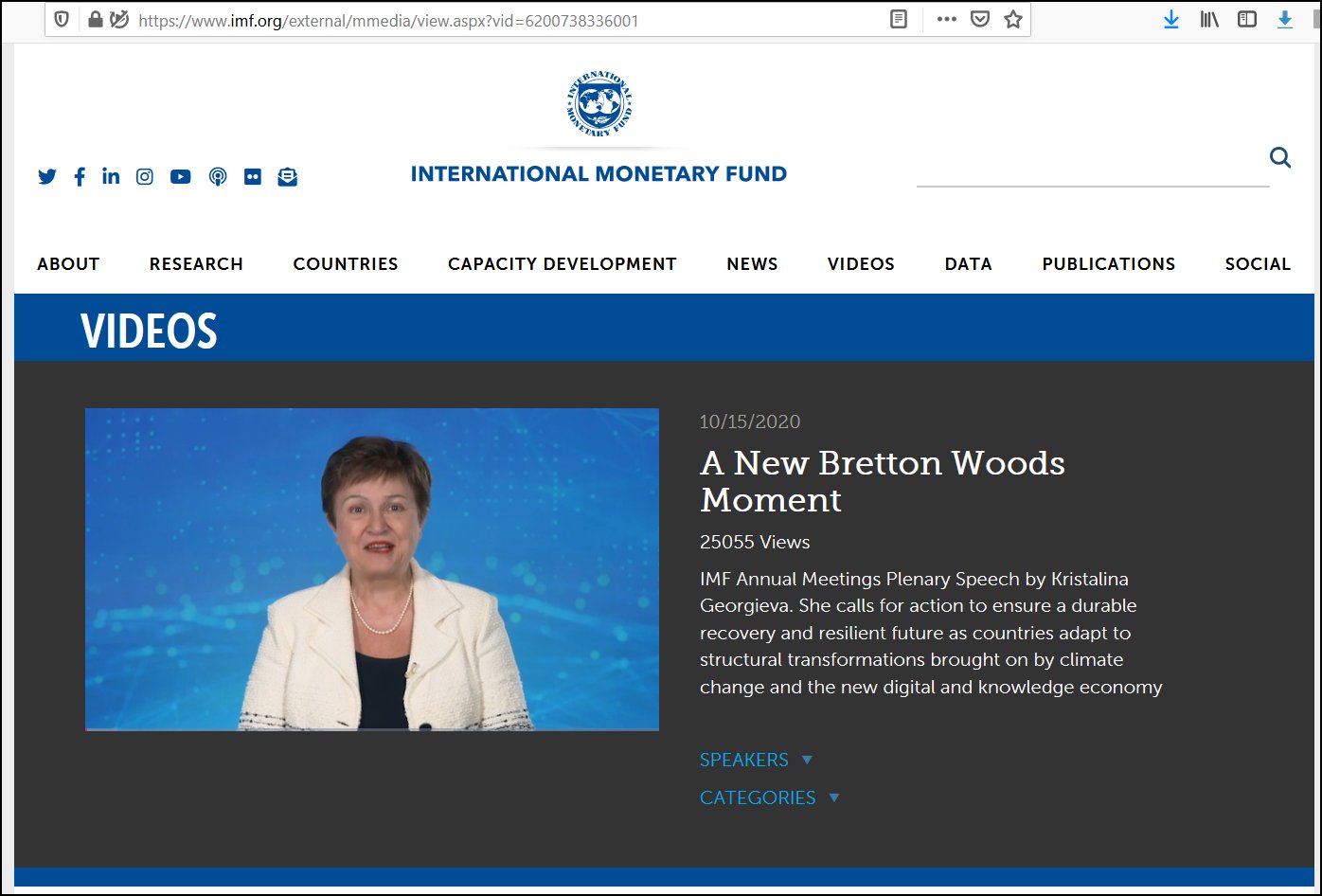

The original IMF video can be found hereunder should you wish to watch it in full.

Video URL: https://www.imf.org/external/mmedia/view.aspx?vid=6200738336001

Now, I think that Simon covered just about everything in his analysis. However, there is one point I think he missed. I am talking about some particular language that the IMF's Managing Director - Kristalina Georgieva uttered during this speech for the ages, namely the following (taken from the transcript of the speech):

In the first section 1. Introduction: ‘A sisterhood and brotherhood of humanity’:

"...But it is a climb up. And we will have a chance to address some persistent problems — low productivity, slow growth, high inequalities, a looming climate crisis. We can do better than build back the pre-pandemic world – we can build forward to a world that is more resilient, sustainable, and inclusive".

Two things here folks. First, she mentions the "looming climate crisis. In technocrat speech that translates (and signals to her cronies) that the new system will be tied/integral to one that will ensure banking institutions (such as the IMF and others) play ball with regards to further taxing and looting governments and corporations (and, indirectly, all individuals) on the back of a fake climate crisis as has been nefariously devised by former Bank of England Governor Mark Carney which I've outlined and exposed nearly a year ago.

Next, the IMF head uses the words resilient, sustainable, and inclusive - all of which are technocratic code words that are often used in UN Agenda 2030 and their Sustainable Development Goals - which we all know are the Elites' ultimate power grab and worldwide enslavement mechanism. I won't elaborate on this particular scheme, as others have done a really good job at it.

I will only say that this particular "New Bretton Woods" style reset is aligned with this greater UN agenda as well as with the WEF (World Economic Forum's) the Great Reset. For an excellent backgrounder on the WEF - read Technocracy: The Digital Panopticon Of The World Economic Forum.

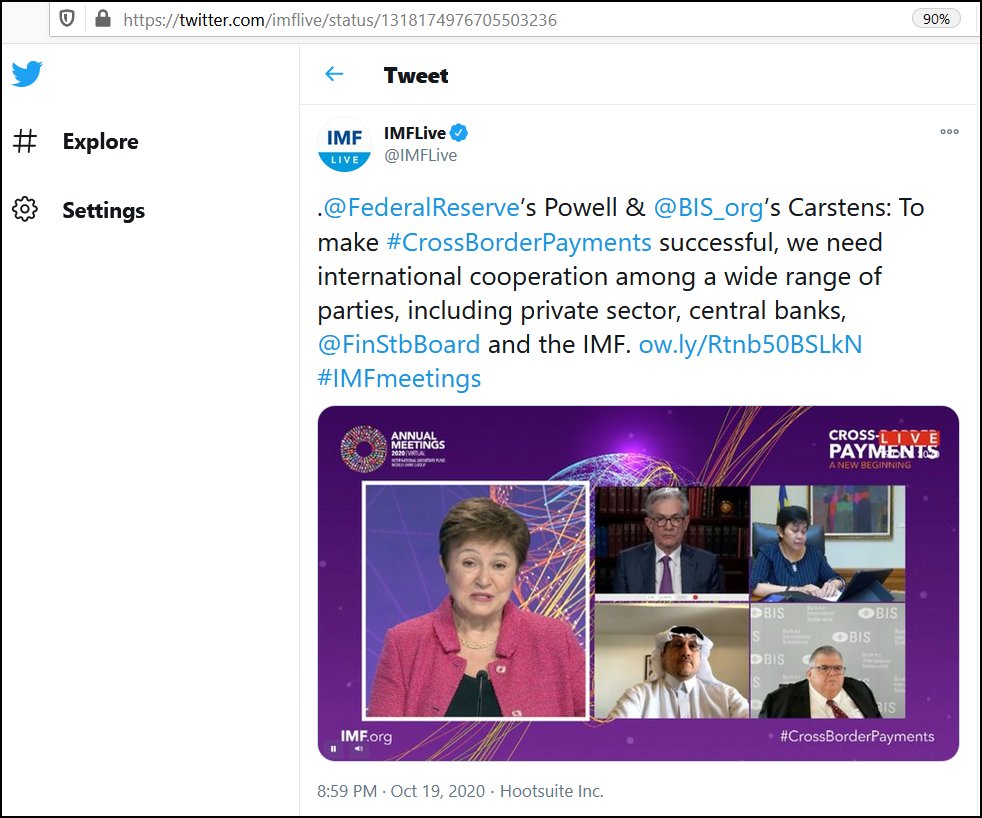

The IMF has a Twitter account and has tweeted the following regarding this New Bretton Woods Reset:

IMF Tweet, October 19, 2020

And merely one key reply that sums up all human sentiment:

But also notice that in the first line of the Tweet she includes both Powell from the US Fed and Carstens - the head of the BIS (Bank for International Settlements) and that the IMF needs "international cooperation" among not only central banks but also the "@FinStbBoard" (Financial Stability Board, i.e, the financial regulatory authorities) and of course the BIS. "Cooperation" signals that they will be colluding with all of these parties and many others for the desired implementation of this new monetary system.

At the very least, we need to have a look at both the BIS and the US Fed which we will do below.

But before we do that, you should also check out an October 19 post by the IMF entitled A Leap Forward on Cross-Border Payments which is also highly relevant to this monetary reset.

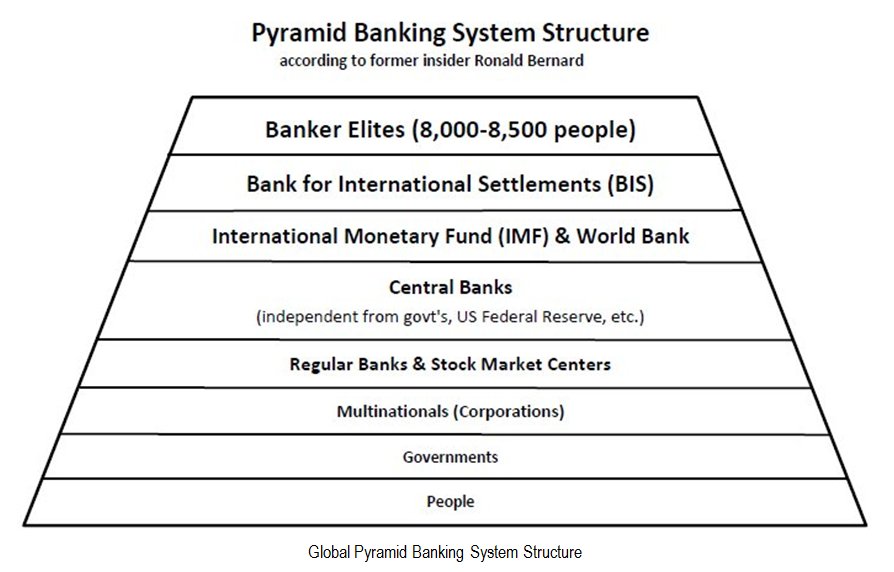

BIS (Bank for International Settlements)

Any analysis of CBDCs and a Monetary Reset would be useless if we do not carefully examine what the BIS is up to. For the BIS, though very quiet and under the radar, are the most commandeering of all financial institutions.

The BIS is the central bank of central banks.

But who exactly is the BIS. In my four part series on the International Banking Cabal, I laid bare all the ugliness that is the BIS. Similar to the IMF, it enjoys total immunity from prosecution at is headquarters (located in Basel, Switzerland) which, like the City of London or Vatican City, resides in its own separate and sovereign territory. It abides solely by its own charter and statutes enjoying complete immunity from any prosecution, government, or legal authority. They are untouchable. Or as former elite banker Ronald Bernard puts it:

“… they are above all worldly rules, nobody can touch them, they have complete immunity. So they have a complete immunity for everything on earth.”

He then goes on to elaborate further:

“Furthermore they have their own police service, so you can’t just go in yelling ‘You bastards!’ or something of the sort, because you won’t get away with it. To be concise, it’s a fully recognized, immune state, beyond the grasp of any rules. Inviolable. ”

You can read more ugly background details should you wish to in Part II - The BIS of my series; it's definately worth the read if you can spare the time.

Now, with that out of the way, what is the BIS up to lately with regards to CBDCs and this new Moneraty Reset?

Allow me to use 3 sources for this. The first is an article from Cointelegraph.com - a premier news outlet for all things crypto. The other two sources are taken directly from the BIS's own website.

With Central Bank Digital Currencies a point of focus across the globe, a number of countries' banking authorities have jointly produced a document discussing the currency type at length.

The Bank for International Settlements told Cointelgraph in a statement that a group of seven central banks and the BIS had collaborated on the report, "identifying the foundational principles necessary for any publicly available CBDCs to help central banks meet their public policy objectives."

The Bank of England, the U.S. Federal Reserve and the Bank of Japan sit among the governing bodies involved in crafting the document, titled: Central bank digital currencies: foundational principles and core features.

Notice that these 3 banks are major ones and the other four will be mentioned a bit later.

The document clarified that vital components of sound CBDCs include convertibility, convenience, security, speed, scalability, legal soundness and several other categories.

Though this article in istelf doesn't reveal much in terms of what the BIS is up to, it can give us an indication of who some of the power players are and which "blocks" (allies) are working together.

Of the 7 countries mentioned, they include the following central banks (note that 7 countries is misleading, as the EU is counted as one but in fact is comprised of many countries):

- The Bank of Canada

- The European Central Bank (ECB)

- The Bank of Japan

- Sveriges Riksbank of Sweden

- The Swiss National Bank,

- The Bank of England

- The Board of Governors of the Federal Reserve (United States)

Most notably, these represent the 6 of the 7 most traded currencies in the world. (and the Swedish Krona is the 9th most traded)

Let me repeat that: these represent the 6 of the 7 most traded currencies in the world.

Now, if that is not significantly telling, then I don't know what is.

The first publication from the BIS which is related to the Cointelegraph article above is the following:

- BIS - Central bank digital currencies: foundational principles and core features (09 October 2020)

These 7 central banks are coordinating with each other via the BIS. In other words, the BIS is directing policy, coordination, and future actions for these central banks - all of which have the same (or nearly the same) owners (i.e., rich families, big banks, and select corporate conglomerates).

This is were the real world power lies, folks.

Image source

The BIS sits near the top of the banking pyramid and dictate to the IMF, the Central Banks, and Governments what their marching orders will be.

Accordingly, we need to pay our utmost attention to this group and whatever information they are willing to share with the public; mind you, there is obviously a lot more happening behind the scenes that they are not sharing with us.

Should you wish to read what they are willing to share, you can have a look at this document entitled Central bank digital currencies: foundational principles and core features (PDF).

They have also published a video (Media briefing on CBDC publication) should you wish to watch it. Note that this video which appears on the BIS's own on YouTube channel has the comments disabled so viewers cannot add comments about it. Surprise surprise. I wonder why...

Another BIS speech publication worthy of our attention is the following :

- BIS - Burkhard Balz: Digital currencies, global currencies (20 October 2020)

Bukhard Balz is a member of the Executive Board of the Deutsche Bundesbank from Germany.

As Germany represents the "financial head" of the EU and the ECB, any statement coming from him should carry a lot of weight and consideration.

Balz raises some extremely salient points in his speech which I will offer hereunder along with my key takeaways for each [emphasis added]:

At the same time, we must also keep an eye on the risks that could potentially come with the issuance of a digital euro given its design.

Note that as a German banker, he is representing the interests of the EU and the Euro.

For example, depending on its characteristics as a store of value, depositors might transform their commercial bank deposits into liabilities of the central bank. This might lead to the structural disintermediation of the banking sector and, as a consequence, could potentially dampen the provision of bank credit to the economy.

This is banking tech talk for a few things. By "structural disintermediation of the banking sector" I think he means the the banking sector can become destabilized should depositors withdraw deposits for digital Euros which would remove them from the banks' balance sheets, thus becoming liabilities.

In other words, **if the funds are not on deposit, debt (credit) cannot be issued to others - this is the bread & butter of the traditional fractional reserve banking system. Or put simply, if every unit of a digital currency is accounted for on a blockchain it can't be used for funny business as is done in the current fractional system.

This is the core dilemma these banksters face with the issuance of CBDCs. And it is something, ultimately and welcomingly, that will be to our advantage.

What if, in times of crisis, bank deposits were rapidly withdrawn and converted into a digital euro? We call this scenario a "digital bank run". The result could be the destabilisation of the entire financial system.

This is an crucial observation on the part of Balz. We know about bank runs. In the past, bank runs, like the one in the movie It's a Wonderful Life, happens very slowly as depositors line up at the bank in the hope that they can retrieve all or at least some of their funds.

In the digital world, however, bank runs could occur amazingly quickly which could wipe out banks in a matter of minutes, if not seconds.

I bet you anything that Balz caugt the unswerving attention of all attendees to his speech with this statement. (I'm sure some may have either threw up a bit in their mouths or sprung a leak in their trousers.)

Therefore, we might need to consider introducing tools to ensure that a potential digital euro would mainly be used as a means of payment, but not as a store of value. One option to be investigated would be to allow users to hold digital euros only up to a threshold at any given time.

"Tools" to ensure that a digital euro can only be used as a means of payment but not as a store of value would be one heck of a smoke-and-mirror trick. But, believe you me, I am certain there are people hard at work at the BIS and in dark corners of central banks working on this conundrum. These cunning banksters are financial engineers of the highest order; so, don't be surprised if they come up with a creative way to circumvent this dilemma.

We should also be aware that the availability of CBDC to foreign citizens could come with substantial consequences for the issuing country.

Of course, we live in a highly and integrated globalized world; therefore, multiple parties will wish to own foreign digital currencies. The question is, what will they (foreigners) eventually be allowed to own - the digital currency itself from the issuing nation (or block), or something else?

He then continues on this point:

For example, it could result in a revaluation of its own currency, but also for other countries, if it leads to fears that their own monetary sovereignty might be negatively impacted. That speaks, in my point of view, in favour of close and open cooperation between the major economies in the world.

Bingo. For once, an honest banker speaks and fails to disguise his rhetoric in insider-lingo reserved solely for bankster cronies. Thank you for the heads up Mr. Balz!

So, what he's suggesting here - "open cooperation between the major economies in the world" essentially means what I suspected all along.

Namely, that these 7 central banks (and most likely other nation blocks) will be forced by the BIS to fully "cooperate" or coordinate the operations of their respective CBDCs in a manner so as to permit the synchronized issuance, deposit, retrieval, re-evaluation, appreciation, depreciation, or bebasement of their respective digital currencies to keep them "elbow-locked", so as to keep the entire monetary ecosystem afloat.

This is the direction in which I surmise the BIS will take with regards to the issuance of CBDCs.

You see, this is precisely what they've been doing in the last several years with regards to "QE", or debasement of their currencies; if they all do it more or less in unison, it doesn't appear that any particular one of those currencies is becoming weak (with the exception of when they are compared to gold, of course). These central banks are still employing this collusive tactic to this day. And that is why they are so desperate to continue the charade post-CBDC issuance.

Regional & Country-specific Notes of Interest:

China:

I put China first here, not because of any alphabetical order, but rather because when it comes to CBDC, they are miles ahead of the curve, practically ready to officially launch at a moments notice.

Having lived in China since 2008, I have a very intimate view of how things are developing in this enigmatic nation.

China, and more specifically its central bank the PBOC (People's Bank Of China), has been working on its CBDC for many years now. And it has been tested extensively and is in trial runs in major cities such as Shenzhen for a while now.

Moreover, they have even recently launched a pre-run of the CBDC, or digital Yuan (as it is also called) directly to citizens via a digital wallet on their smart phones. More specifically, they have offered "free money" (a couple of hundred Yuan) to those willing to try the wallet for purchases at select participating merchants.

Of course, the idea here is to entice citizens to onboard them into the new system.

And it has just been announced that the Chinese CBDC will not compete with Wechat Pay and AliPay, as these will merely serve as wallets to store digital Yuan. This will serve as a good indication as to how other countries will treat their own domestic payment systems (i.e., more as service wallets).

What should most be examined by the Chinese CBDC, or digital Yuan, though is the mechanics behind the system. How will the digital Yuan [tokens?] be distributed, transacted, monitored, and controlled?

In a country like China where the government wants to control everything, the issuance of a CBDC is no exeption. In fact, once implemented it will be able to aggregate an even scarier amount of control over their citizens and any company or organization in China, and arguably those elsewhere who interact with China.

If you want to get a crystal clear idea of what the Chinese CBDC will look like, look no further than the following superb article written well over a year ago (May 17, 2019) but still extremely timely and relevant to what I see occurring on the ground today:

- Coindesk - Digital Renminbi: A Fiat Coin to Make M0 Great Again by Dovey Wan.

This is a superb article that will show you exactly how the Chinese government and its central bank will benefit from the new monetary standard.

Lastly, the mechanics of the Chinese CBDC system is the "wet dream" of what other CBs around the world can only dream of implementing (though I'm sure they will try their darndest to duplicate), for the level of control it has is quite dystopian and Orwellian to say the least.

European Union:

As I mentioned earlier when scrutinizing the BIS's role in all of this is that Germany is central to the EU. The remarks by Bukhard Balz from the Executive Board of the Deutsche Bundesbank are really key to understanding the direction the EU will take with regards to issuing its own digital Euro.

One primary concern for Balz was how the revaluation currencies may occur with cross-border ownsership and flows.

This is why the idea of "stablecoins" worries him, and rightly so. Here is a relevant article that reiterates and expands upon this concern:

- Cointelegraph - Chasing the hottest trends in crypto, the EU works to rein in stablecoins and DeFi (Oct. 18, 2020)

"Stablecoins are widely considered to potentially bring significant benefits as a digital method of payment, providing for greater financial inclusion and a more efficient method of transferring funds. They are also viewed as a potential risk to financial stability and integrity and could dilute the effectiveness of monetary policy. It would appear logical that the European Union may not welcome an entity other than the European Central Bank issuing Euro in an electronic format."

The key part here is "the European Union may not welcome an entity other than the European Central Bank issuing Euro in an electronic format."

In other words, any stablecoin representing the Euro would be enemy #1 and a major threat to their envisaged CBDC system.

Accordingly,

"Illustrating the depth of the top EU officials’ concern over preserving the union’s monetary sovereignty is the fact that, earlier in September, “finance ministers of Germany, France, Italy, Spain and the Netherlands issued a joint statement outlining that stablecoin operations in the European Union should be halted until legal, regulatory and oversight challenges had been addressed,” said Konstantin Richter, CEO and founder of the blockchain infrastructure company Blockdaemon."

It is quite understandable to see why they would want to ban stablecoins, for other entities issuing euro backed- or pegged- stablecoins would indeed pose a threat to them.

Stablecoins are generated and made available on cryptocurrency exchanges and in the DeFi space. CASPs - Crypto Asset Service Providers - are parties that make stablecoins available.

Another major source of uncertainty is the requirement for all crypto-asset service providers, or CASPs, seeking authorization to operate in the EU to be legal entities with an office in one of the member states.

Whether the European authorities will treat individual DeFi apps as CASPs remains an open (and central) question, but if this is the case, developer teams maintaining DeFi protocols might be forced to come up with workarounds that will stretch the notion of “decentralized” incredibly thin.

[Elsa Madrolle, international general manager at blockchain security company CoolBitX] thinks that at that point, DeFi projects will fall into one of two categories — regulated and unregulated — and the big question will be whether the rest of the world will align itself with the European framework.

Simply put, some DeFi CASPs or stablecoin providers will have to be crafty so as to avoid falling into the radars of EU financial regulators and authorities. But highly decentralized ones may prove more effective. This can be sustantiated by the following exerpt from this same article:

Nathan Catania, a partner at XReg Consulting — a regulatory and policy firm that has recently published a breakdown of the proposed regulatory framework — is hopeful that it is possible for regulators to reconcile MiCA requirements with not regulating DeFi out of existence. Catania said:

"I believe that a project which is sufficiently decentralized and does not provide the service on a professional basis to a third party cannot be considered a CASP and there is still room for DeFi projects to exist."

The issue covered above is but one of many and the EU machine is one big enigmatic and bureaucratic mess. So, it is difficult to know what will come out of this transition into decentralized finance and digital currencies.

My bet is that given the bureaucratic and slow-moving nature of policy issuance, approval, and implementation will put the EU, as a whole, at a disadvantage and the DeFi space at an operational advantage to better serve the needs of those wishing to transact and exchange in a Euro CBDC or digital Euro clone.

The US & Federal Reserve

An October 19 article from ZeroHedge entitled Powell Lays Out The Key Reasons Why The Fed Is Moving Toward Digital Dollars nicely encapsulates how the Fed, or at least the powers behind this powerful financial institution, are posturing in this mighty game of deception.

The Fed and CBs have always been masters at deception. Smoke and mirrors, spinning plates, you name it, they've got it all covered. Their level of deception is unmatched and this time is certainly no exception.

The article begins with a superb collection of recently written works on the Fed's latest moves:

Did The Fed Just Reveal Its Plans For A Digital Dollar Replacement?

House Stimulus Bill Creates "Digital Dollar" To Send Virus-Aid To The 'Unbanked'

The Fed Is Planning To Send Money Directly To Americans In The Next Crisis

ECB Trademarks "Digital Euro" As It Begins Experiments On Digital Currency Launch

The Circle Is Complete: BOJ Joins Fed And ECB In Preparing Rollout Of Digital Currency

The article "In Unprecedented Monetary Overhaul, The Fed Is Preparing To Deposit "Digital Dollars" Directly To "Each American" is worth mentioning again. If you know how the current debt-based fiat monetary system works, you know that for it to continue, currency has to be perpetually created in larger and larger amounts, otherwise the whole system collapses.

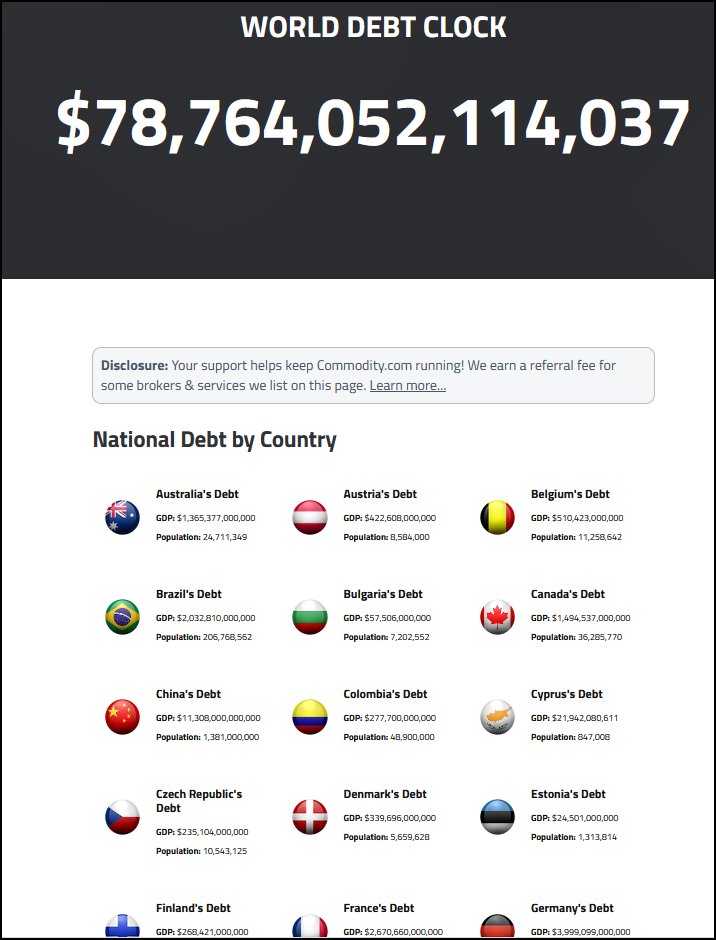

Accordingly, the Fed (and other CBs) have to create more and more debt (issue more currency into circulation by increasing the money supply). This has, of course, led the world into monumental debt:

World Debt of US$78.7 trillion as of 2020-10-25, source: https://commodity.com/data/debt-clock/

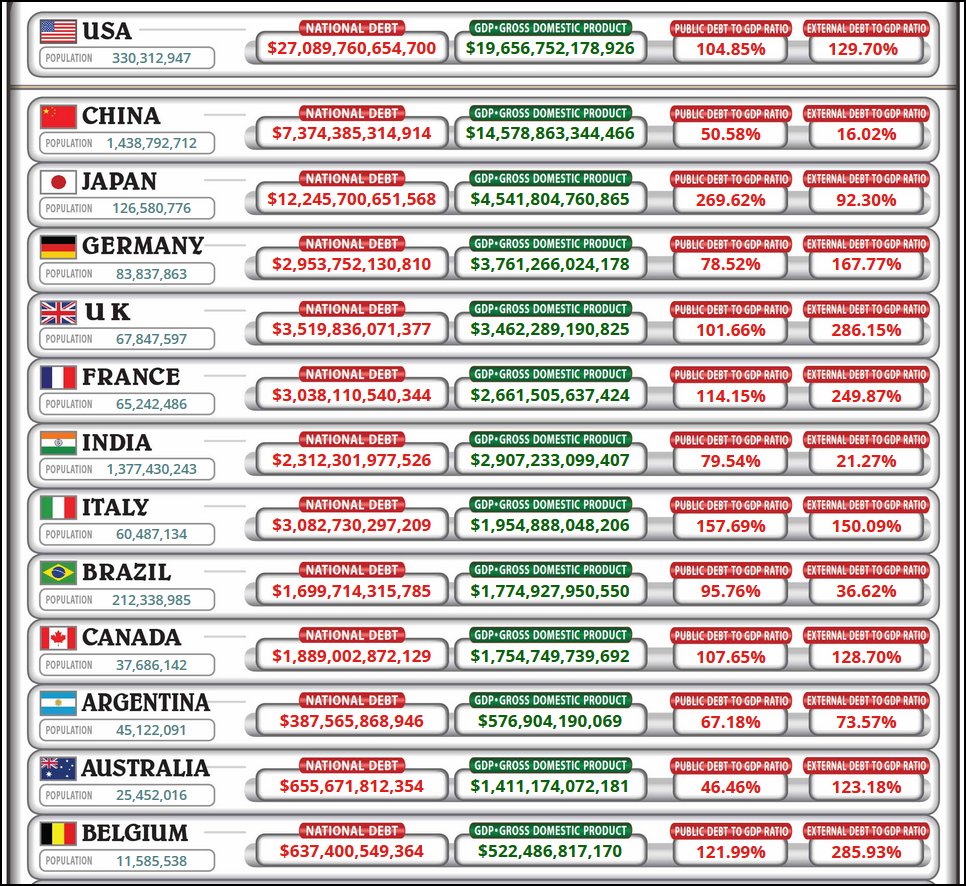

Select G20 countries' Debt levels as of 2020-10-25, source: https://usdebtclock.org/world-debt-clock.html

The two screenshots of global debt above are scary to say the least. This is national debt that has been accumulated over decades and are liabilities of every citizen of the respective countries as well as their children, grandchildren, and future generations.

In short, this is the result of a reckless monetary system that has financially enslaved the masses for way too long. The Central Banks are the main culprits of this thievery and its a damn shame we let them get away with it.

Do you want more of the same in the future? Or, do you want something else for you, your children, your family, and your country?

On the back of the Covid-19 Scamdemic, the Fed has increased the money supply by over $3 trillion in just a few months.

In the current election fog, there is talk of additional "stimulous" (stimulus is a smoke-and-mirror term that simply means they will print more money out of thin air to inject into the big banks and stock markets) either through monetary policy or fiscal policy.

Monetary policy has traditionally been enacted by CBs and is usually in the form of changing interest rates and increasing (or decreasing) the money supply.

Fiscal policy is usually enacted by the legislatures of the countries (in the US this is Congress) - something that is usually not in the control of CBs.

But this time, if a CB can issue a CBDC and deposit it directly into citizens' bank accounts, this can act as a Fiscal Policy measure (much like when a legislature votes in a "stimulous package", to reinvigorate a faltering economy).

If the Fed (or any other CB) deposits funds directly into citizens' (and corporations') accounts, they are in effect bypassing or governments legislatures altogether. In other words, they are usurping sovereingty of the nations. This is no less than a Financial Coup by the banksters.

Sorry to have gotten side-tracked again. Back to the article in question:

... and the main reason cited by Powell: "reaching consumers who have been traditionally underserved by financial institutions", which is another way of say granting the Fed permission to make targeted direct deposits to virtually anyone, anywhere in the world at any given moment in time, in the process making obsolete such legacy institutions as Congress, Commercial Banks and the IRS, since the Fed has ultimate control over the lifespan of every single currency unit from inception to its eventual destruction at the hands of the Fed.

This passage goes along with what I said previoulsy in that it could basically eliminate legislatures and even commercial banks - those we use to deposit our funds and pay our bills.

That said, while CBDCs are clearly coming, we expect a period of at least several years before their arrival, absent another major financial crisis, of course: "We have not made a decision to issue a CBDC and we think that there's a great deal of work to be done", Powell said.

Another very astute article on the Fed entiteld BofA: Fed Will Use Digital Dollars To Unleash Inflation, Universal Basic Income And Debt Forgiveness is also worth a read and further confirms the fact that the Fed (and other CBs) would unleash even more debt and inflation on the masses.

Canada & the Bank of Canada:

Canada has also been working on a CBDC for a number of years now. They have also done extensive examinations on its effects and integration with domestic payment systems. One only needs to do a search with the terms "Jasper" to find out more.

One of my main takeaways for Canada is that they seem to be taking a wait-and-see approach as to what precise kind of CBDC they will issue and how it will be tied to the domestic payment systems.

Most likely, they are waiting for orders from their superiors in the upper echelons of the banking cartel (mostly the BIS) before proceeding.

The subservient Canadian government has a track record of being a player that goes along with anything the G20, City of London, and supranational institutions such as the BIS and IMF have in the pipe.

Here are a few notes of interest that have crossed my radar in recent times:

- Cointelegraph - Bank of Canada Prepares for Digital Currency “In Case One Is Needed” (Feb 25., 2020 )

“If one or more alternative digital currencies threatened to become used widely as an alternative to the Canadian dollar, then a central bank issued digital currency could be used to defend monetary sovereignty.” - Bank of Canada Deputy Governor Tim Lane

- Bank of Canada - Security and convenience of a central bank digital currency (PDF):

"An anonymous token-based central bank digital currency (CBDC) would pose certain security risks to users...The central bank could mitigate these risks in the design of the CBDC by limiting balances or transfers, modifying liability rules or imposing security protocols on storage providers." (Abstract, p. 1)

The last cited passage is particular interesting. I am not exactly sure how a bank could design and use a CBDC and limit balances and transfers. Sure, it could be done on a technical level, but this would be a whole can of worms should they decided to implement such restrictions.

Continue reading Part 2

It includes the last two sections:

- Thoughts and Predictions on this Global Monetary Reset

- Final Thoughts

Excellent information for those of a mind to acquire it. Given I am not going to avail myself of any CBDC, as I have largely done without fiat for the last decade, I reckon a simpler message may be more difficult to poison with disinformation - the forte of the globalists - and be more easily understood by folks concerned about the survival of their freedom.

CBDCs can be completely controlled centrally, and turned off if folks don't kneel to the policies promoted. Folks dependent on CBDCs will be slaves of policy makers, and will not keep their freedom.

The fact will be that folks will have to have other means of transacting to remain free.

I deal in goodwill, and no CBs can short it, tax it, or steal it. It isn't ideal, because it's only a store of value honorable people recognize, and many people aren't honorable. That's ok though, because I don't want to do business with them as aren't suitable for transacting in goodwill anyway.

Thanks!

Thank you!